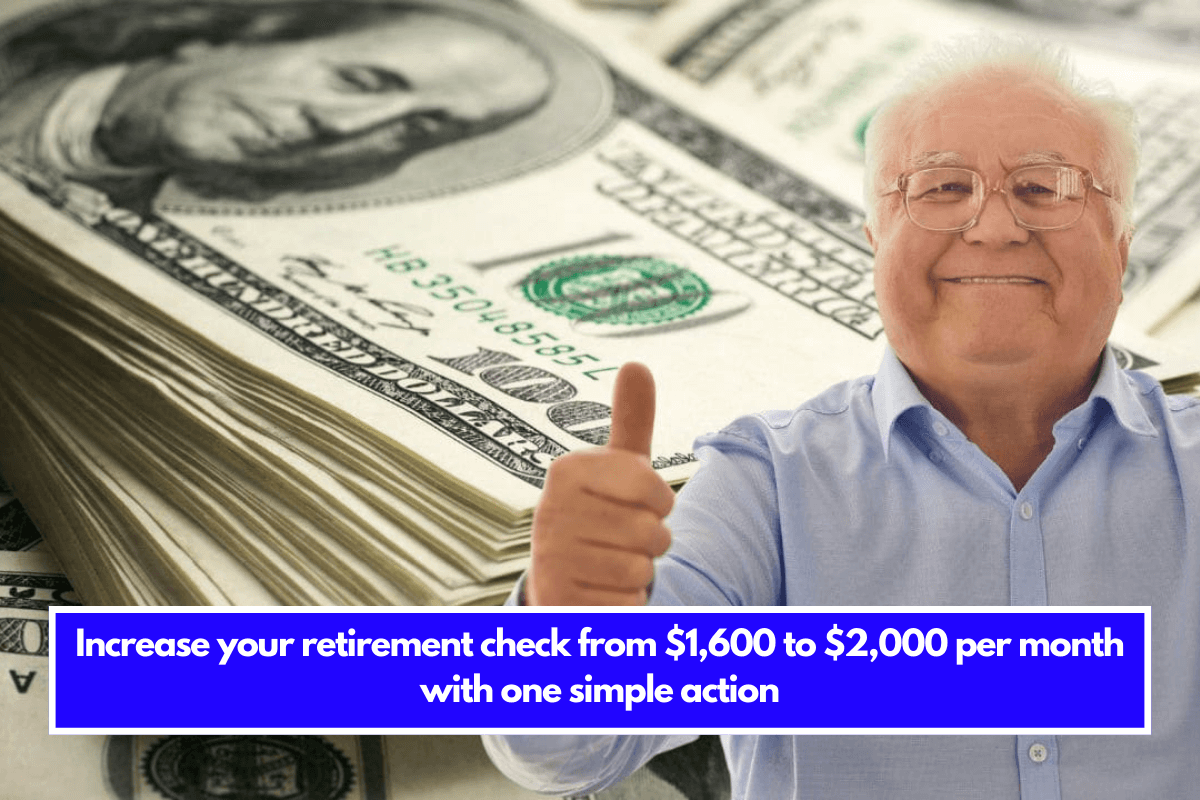

Increasing Social Security retirement benefits may seem hard for many workers in the United States, but a simple step can make a significant difference in monthly checks. People frequently prefer to file for benefits at the earliest allowable age, 62. While this may appear to be an appealing alternative, it can result in a large reduction in monthly price.

In fact, delaying retirement could be the key to receiving a considerably higher monthly check. A person who retires at 62 can enhance their monthly benefit to $2,000 by waiting until full retirement age which is typically 67. This boost provides significant financial relief, which can improve quality of life in retirement.

The Simple Step to Increasing Retirement

To increase your monthly Social Security retirement cheque, delay enrolling for benefits. Starting Social Security payments at age 62 results in a permanent reduction in benefits. Reducing benefits by up to 30% can significantly lower an American retiree’s standard of living over time.

Alternatively, waiting until full retirement age may be beneficial. Most people will need to wait until they reach the age of 67. We will receive 100% of the contributed benefit as a result of the wait. Delaying retirement until age 70 results in higher monthly payments due to Social Security Administration credits for each year of delay.

Retiring at age 67 can result in a monthly income of $2,000, up from $1,600 at age 62. This boost not only increases financial stability in retirement, but it also provides better peace of mind in the face of unexpected needs. However, each case is completely unique, and before making a decision, it is a good idea to review our work history and what the benefit.

Other factors that influence Social Security

Delaying retirement is key for maximizing benefits, but other factors also impact the final amount of Social Security checks. Taking these factors into account can help workers make more educated decisions and earn the most money feasible.

- Years worked: The Social Security Administration calculates the benefit based on the highest 35 years of earnings. If a worker has not accumulated 35 years of work, the missing years are counted as zero, which reduces the average and, therefore, the monthly amount.

- Earned income: The higher the salary during the working life, the higher the Social Security benefit. This is because payments are calculated based on average earnings during the 35 most productive years.

Considering these two elements is critical to ensuring that the monthly Social Security benefit is as large as feasible. In this situation, combining a delayed retirement age with a strong, well-paying work history can mean the difference between a difficult retirement and a more comfortable and secure retirement.

Also See-:- How would a U.S. government shutdown affect Social Security pensions